Core Use Case

Sizing Logic

Most drawdown damage comes from inconsistent sizing, not setup logic. A sizing calculator turns risk from guesswork into policy.

Risk Sizing Tool

Use this calculator to convert stop distance into contract size using fixed risk.

Convert stop distance and risk budget into repeatable position size decisions.

Core Use Case

Sizing Logic

Most drawdown damage comes from inconsistent sizing, not setup logic. A sizing calculator turns risk from guesswork into policy.

AutoTrading

AutoTrading deployment + risk

Use this guide as your rollout checklist before scaling automation.

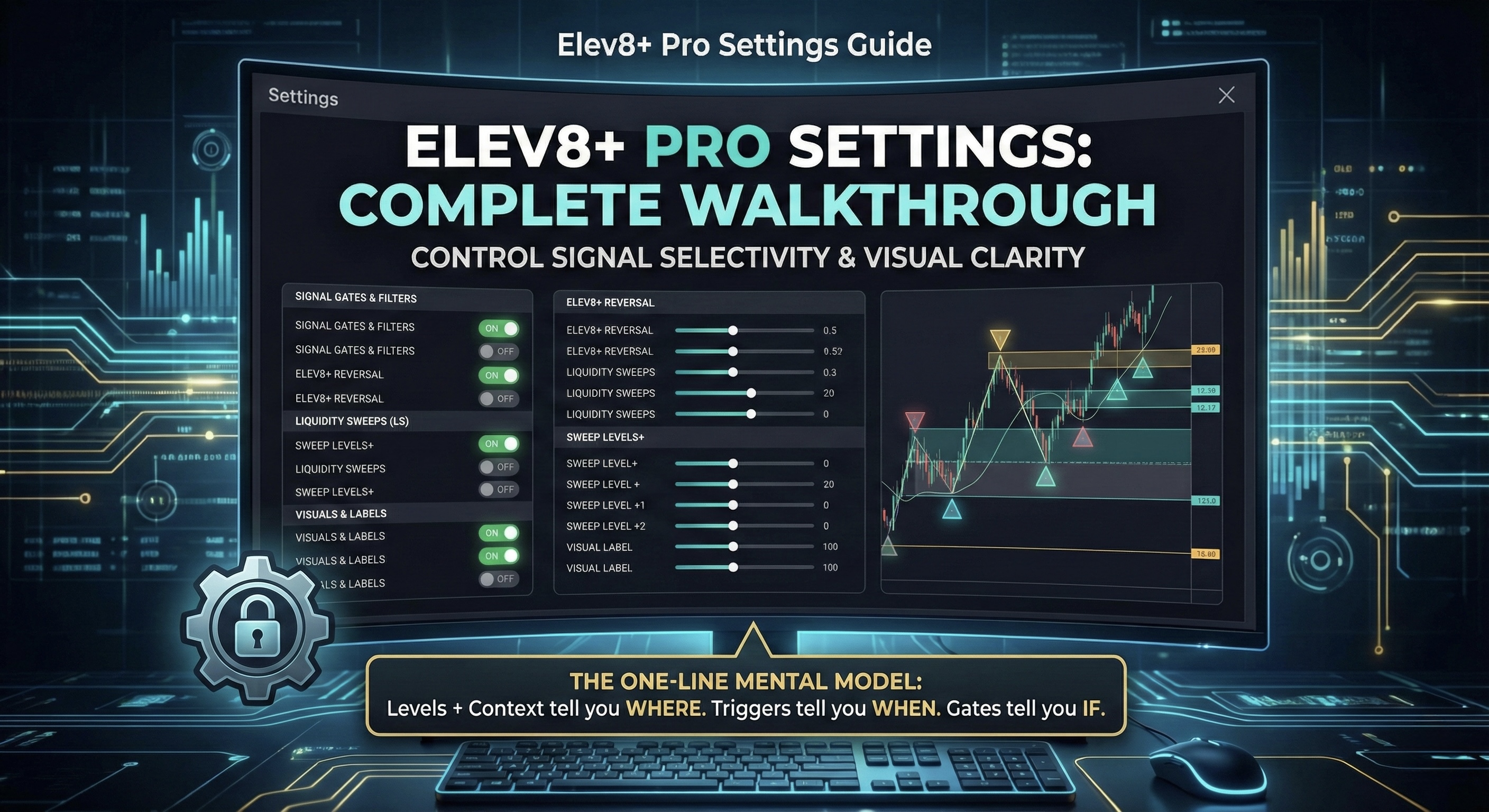

Screenshot context: bot risk-control panel for drawdown and kill-switch logic. This page explains how it fits into a MNQ risk calculator process.

Execution Goal

Convert this concept into a staged, risk-first deployment plan you can monitor and review.

Next Step

Use this page as your launch checklist, then run the same risk-first process in AutoTrading and validate context in Market Health.

Implementation path in AutoTrading

Context filtering with Market Health

Intent Match

Most drawdown damage comes from inconsistent sizing, not setup logic. A sizing calculator turns risk from guesswork into policy.

Why This Helps

Prevents oversized entries.

Why This Helps

Normalizes risk across setups.

Why This Helps

Supports long-run consistency.

Use this as a strict sequence. If one step fails, stand down and wait for cleaner confirmation.

Set fixed dollars or account-percent risk.

Measure invalidation-based stop distance.

Contracts = floor(risk budget / risk per contract).

20 x $2 = $40 risk/contract, so 3 MNQ contracts.

$100 budget, $24 risk/contract, so 4 MNQ contracts.

Enter your risk budget and stop distance. This uses a default of $2 per MNQ point.

Use Market Health for daily setup context, then apply risk math consistently. If you automate later, the same sizing rules become your deployment baseline.

Use this view as a checkpoint when deploying MNQ risk calculator with staged risk controls.

Next Step

Start in AutoTrading for implementation details, then use Market Health to keep entries aligned with current structure.

Deployment checklist + platform setup

Risk gates before scaling